The China social credit system is a broad regulatory framework intended to report on the ‘trustworthiness’ of individuals, corporations, and governmental entities across China. In this introduction, we explain how the China social credit system works in 2024, how it differs from financial credit ratings elsewhere, and how it impacts individuals and companies operating within China.

A társadalmi hitelrendszer egy olyan összetett keretrendszer, amely az egyének és vállalkozások viselkedése, pénzügyi előzményei és társadalmi interakciói alapján értékeli és pontozza őket. Bár leginkább Kínával hozzák összefüggésbe, hasonló rendszerek vagy hitelpontozási mechanizmusok más országokban is léteznek különböző formában. Az olyan online kaszinók, mint a https://kaszinoworld.com/, hatása a társadalmi hitelrendszerre sokrétű lehet, az adott szabályozási környezettől és a szerencsejátékokkal kapcsolatos társadalmi hozzáállástól függően. Azokban a régiókban, ahol az online kaszinók legálisak és szabályozottak, a kormányzati politikák befolyásolhatják a társadalmi hitelrendszerre gyakorolt hatásukat. Egyes országok a felelős szerencsejáték-gyakorlatot pozitív tényezőnek tekinthetik, míg más országok a szerencsejátékot az egyén hitelképességét befolyásoló negatív viselkedésnek tekinthetik.

Key Takeaways

1. The goal of the China social credit system is to provide a holistic assessment of an individual’s or a company’s trustworthiness.

2. The China social credit system, while still in development, is arguably an extension of existing social rankings and ratings in China which have existed for millennia.

3. The consequences of a poor social credit score could be serious. It may affect travel prospects, employment, access to finance, and the ability to enter into contracts. On the other hand, a positive credit score could make a range of business transactions much easier.

4. It is essential that any foreign business consolidating or establishing their presence in China seek professional advice for managing a social credit score. This applies both to individual scores, and the corporate social credit score.

2024 marks an era of stability in the development of China’s social credit system.

By 2022 an estimated 80 percent of provinces, regions and cities had introduced some version of the system, but now that appears to have slowed down significantly.

One part of the social credit system, the ‘corporate social credit rating,’ appears to be especialy advanced: More than 33 million businesses in China have already been given a score under some version of the corporate social credit system.

So, what is the China social credit system? If commentary in the Western media is anything to go by, it is a somewhat mysterious and scary rating system.

In 2018, former US Vice-President, Mike Pence, sounded the alarm bells about China’s social credit system, stating “China’s rulers aim to implement an Orwellian system premised on controlling virtually every facet of human life – the so-called “social credit score.”

Western media outlets have spoken of the “sinister social credit system” and a system of “total control“.

Is there any truth to such rhetoric, and what does all this mean for businesses expanding into China?

In this article, we break down the Chinese social credit system, as it has been developed to date, and aim to separate the myth from reality.

What is China’s Social Credit System?

The term ‘social credit’ (社会信用体 in Chinese and shèhuì xìnyòng tǐxì in pinyin) doesn’t have a precise meaning — rather, it is an intentionally broad and vague term allowing for maximal policy flexibility.

Plugged into a regulatory framework, the ‘China social credit system’ (also knows as ‘China’s Ranking System’) refers to a diverse network of initiatives aimed at enhancing the amount of ‘trust’ within Chinese society.

The goal of the social credit system is to make it easier for people and businesses to make fully-informed business decisions. A high social credit score will be an indicator that a party can be trusted in a business context.

The system began with a focus on financial creditworthiness, similar to credit scores used in western countries, and moved on to include compliance and legal violations.

The eventual ‘end-state’ of the system is a unified record for people, businesses, and the government, which can be monitored in real-time.

In more recent years, policy development for the social credit system has moved beyond considerations of financial creditworthiness and compliance to encompass a broader notion of ‘trust’.

A common theme in the policy documents establishing the social credit system is the term ‘Chengxin‘, variously translated as ‘trustworthiness’, ‘honesty’, ‘integrity’, ‘sincerity’ or ‘morality’, depending on the context.

More specifically, through facilitating trust, the China social credit system supports the following goals¹:

- Financial creditworthiness (zhengxin 徵信)

- As in most countries, firms and individuals need a way of assessing whether others are a safe bet for lending/extending goods on credit. The social credit system aims to rectify this gap in China’s financial and business ecosystem.

- Judicial enforcement (gongsi gongxin 司法公信)

- Enforcement of judicial decisions (such as judgement debts) has proven particularly difficult in China. Part of the purpose of the social credit system is to find new enforcement mechanisms for existing laws and court decisions.

- Commercial trustworthiness (shangwu chengxin 商务诚信)

- This means improving compliance and anti-fraud mechanisms for commercial enterprises, and those who participate in them.

- Societal trustworthiness (shehui chengxin 社会诚信)

- This covers the broader goal in the social credit system of supporting a more ‘moral’ society. We see this goal at work in social credit initiatives which value honesty, hard work and devotion to family.

- Government integrity (zhengwu chengxin 政务诚信)

- The social credit system is ‘self-reflective’: Bureaucrats and politicians themselves will be subject to the regime, with the goal of reducing corruption.

The high-level goals are to be achieved via three key practical mechanisms:

- Data gathering and sharing

- The fundamental building block of the social credit system is data. Through the system, data is gathered by central, regional and municipal government bodies, as well as private actors, and shared. ‘Big data’ algorithms are then used to process that data in a meaningful manner.

- Curation of blacklists and redlists

- The data acquired is used to add individuals and corporations to lists (some public, some not).

- Punishments, sanctions and rewards

- Based partially (but not entirely) on presence in the lists identified above, individuals are punished and rewarded.

The elements of the social credit system outlined above are put into place by a variety of actors:

- Policy direction

- The social credit system is, at the highest level, driven by the State Council, currently chaired by Premier Li Keqiang. This is the most powerful administrative body within the Chinese government. It is assisted in this task by the National Development and Reform Commission (NDRC). This is a macroeconomic policy body, immediately subordinate to the State Council, and has a mixture of what would in other countries be called Treasury and Reserve/Central Bank Powers. The People’s Bank of China (PBoC) also plays a prominent role at the highest policy level.

- Central government and court implementation

- Dozens of central government departments and agencies have implemented elements of the social credit system, especially the blacklists and redlists. Prominent examples include the Ministry of Transport, Ministry of Culture and Tourism and the PBoC.

- The Supreme People’s Court has also introduced an expansive blacklist of debtors under the scheme.

- Regional and municipal government implementation

- It is through regional pilots that the social credit system has largely been implemented, including the ‘model cities’ initiative introduced in 2017 (see timeline below).

- Private company credit ratings and contracting

- Several private companies have developed their own credit systems (such as Alibaba’s affiliated ‘Sesame Credit’), with participation being voluntary. Some of these have been developed independently, while others have been developed as part of government trials.

- In other cases, private companies have been contracted to provide the infrastructure supporting the credit system such as Baidu’s refresh of the ‘Credit China’ webportal, and Tencent’s development support for the app.

History and Background of the Chinese Social Credit System

While the introduction of a unified China social credit system was formally announced in 2014, precursors to the proposed social credit system have operated within China for centuries — arguably millennia. The idea, or philosophy, behind social credit, might be traced back to the ‘warring states’ period of Chinese history. At that time, various schools of thought competed for dominance:

- Confucianism

- Confucius (551–479 BCE) advocated a ‘holistic’ conception of human nature where individual well-being was connected to good character, and the proper functioning of society as a whole.

- Mohism

- Mozi (470 BC–391 BCE) suggested that all humans should care for each other equally, and advocated a society where all were treated impartially.

- Legalism

- This school, (approximately 400-300 BC), emphasized the importance of laws, strictly enforced from above, in order to preserve social order.

Though arguably ‘legalism’ won out, all three of these schools influenced the first imperial ‘Qin’ dynasty (221-206 BC). It is within this dynasty that a meritocratic assessment and promotion system was applied across the imperial bureaucracy in order to achieve a well-functioning Chinese state. Arguably, this was a rudimentary ‘social credit system’, albeit one applied only to civil servants, and without a precise ‘score’.

In the 20th century, public record systems have been developed to record the behavior and actions of ordinary individuals. For example, the hukou system, in place in its modern incarnation since 1958, registers households, controls internal movement within China, and assigns benefits to households depending on their rural or urban location.

The dàng’àn 档案 is a set of records related to an individual within China, recording that individual’s “performance and attitudes”. This file contains a range of information such as physical characteristics, photographs, employment records, academic records, workplace appraisals, convictions and administrative penalties. This file follows an individual for life, and two copies are held: One is kept by the Public Security Bureau and the other by the individual’s work unit.

This file has been used (and still is) for a range of decisions affecting an individual, such as promotions and access to passports.

A key proposed benefit of the new unified social credit system is that, instead of relying on a paper record to manage society, the electronically-integrated system would expedite the analysis process and make oversight easier.

Timeline of the Development of the China Social Credit System

In 1978-1979, the reforms of Deng Xiaoping opened up the Chinese economy in various key ways, including the “Open Door” policy that permitted foreign investment in China once more. From that point on the lack of traditional credit rating systems, as well as significant corruption scandals, have been seen as a limitation on economic prosperity.

By contrast, developed western economies like the United States already had computerized credit analysis by the 1960s (though scoring systems, such as the FICO, did not rise to prominence until the late 1980s).

We set out the development timeline for the social credit system below:

- Mid-1990s — First credit databases constructed

- The PBoC developed an early database providing financial credit information to commercial banks.

- This was formalized in the ‘Banking Credit Registration and Reference System’ (sometimes translated as ‘Bank Credit Registry and Consulting System’), established in 1997.

- 1999 — The idea surfaces

- Then Premier Zhu Rongji assigned a research team at the Institute of World Economics and Politics of the Chinese Academy of Sciences to investigate solutions to corrupt market behavior. In response, The National Credit Management System² is released, advocating a centralized system, bringing together data from across China.

- The focus of the system at this stage was economic: Debt default, contractual breach, and regulatory non-compliance were to be the key data for the system.

- From this point on, embryonic pilot testing of the system began. For example, in 2000, Shanghai introduced a credit system which assessed eligibility for loans by individuals based on payment of utility bills.³

- 2004 — Official endorsement from the leadership

- Then President, Jiang Zemin, endorsed the social credit system at the 16th CPC party congress in his report ‘Build a Well-off Society in an All-Round Way and Create a New Situation in Building Socialism with Chinese Characteristics’.

- The stated goal was to establish a social credit system compatible with a modern market system.

- In addition, trials on a consumer credit reporting database began with 23 state-owned and commercial banks across seven municipalities.

- 2006 — Credit Reference Centre established

- The Credit Reference Centre was created to be a nation-wide, independent, credit reporting agency.

- Banks were required to start reporting on customer creditworthiness. Through collaboration with government departments and the Supreme People’s Court, additional information relevant for creditworthiness began to be reported.

- 2007 — Co-ordinated national policy development

- The Joint Inter-ministerial Conference on Social Credit System Construction (the ‘joint conference’) was set up to co-ordinate the development of the system.

- Participants include key government departments and agencies such as the Ministry of Finance, the State Administration for Industry and Commerce, and the Ministry of Public Security.

- But members were also included from the Central Commission for Discipline Inspection (the chief anti-corruption body in China), the Central Guidance Commission on Building Spiritual Civilization (the chief ideological body in China, aimed at a “socialist harmonious society”), and the Supreme People’s Court.

- This wide membership beyond traditional government departments is perhaps indicative of the all-encompassing nature of the planned social credit system (and the move from a focus on financial creditworthiness, to broader conceptions of ‘trust’).

- 2009 — Regional pilots of the social credit system commence

- One of the most well-cited cases was the system introduced in Suining county, Jiangsu province. Individuals were given 1000 points, with the ability to gain or lose points based on their behavior. Convictions or debt non-repayment, for example, meant point deductions.

- These points were then used to create a letter grade from A to D. And the result of those letter grades affected employment opportunities, access to business licenses, and eligibility for government support.⁴

- A more recent example is the ‘Social Credit Card’, introduced in Nanjing in 2016. This offers select benefits to individuals with a high social credit score, including discounts and preferential treatment by financial institutions. Assessment criteria include such considerations as the individual’s willingness to donate blood, and whether the individual is recognized as a hard worker.

- 2013 — Supreme People’s Court debtor blacklist established

- This list publishes the names and ID numbers of defaulters.

- As well as the ‘shame’ associated with being on the list, defaulters were prevented from a range of ‘high-end’ expenditure, including traveling and staying in certain hotels.

- Notably, it applies to both individuals and the legal representatives and officers of companies in default.

- In 2017, it was estimated that 8.8 million debtors had been added to this list.

- 2014 — Release of key planning and co-ordination document

- The State Council released ‘Planning Outline for the Construction of a Social Credit System (2014-2020)’ in 2014.

- This document is a culmination of the work of the joint conference, and has guided the social credit system in its development over the past six years.

- Five objectives for the system listed in that document included establishing necessary laws and regulations for social credit, the completion of a credit investigation and sharing system for all of China, developing credit supervision systems, a market for credit services, and establishing mechanisms for keeping trust and punishing those who fail to do so.

- A significant emphasis with this last objective was the development of blacklists and redlists (these are discussed in detail below).

- 2015 — National Credit Information Sharing Platform (NCISP) and private provider trial

- The NCISP is overseen by the NDRC in conjunction with dozens of other government departments. It integrates all the regulatory data used to construct blacklists and redlists.

- It is this database that the Unified Social Credit Code uses to pick out a particular corporate actor.

- Also in 2015, the PBoC authorized a trial for 8 companies to test numerical credit score systems, based on repayment, purchase history and personal characteristics. The most well-known was Alibaba-affiliated ‘Sesame Credit’. These licenses were not renewed, and instead, the 8 companies received a stake in a unified credit platform named Baihang, with a significant stake controlled by the PBoC.⁵

- 2016 — Progression on blacklists and redlists

- 2016 saw the State Council emphasize the standardization of blacklists and redlists (see ‘Guiding Opinions on Establishing and Improving the Joint Incentive System for Trustworthiness and Joint Disciplinary System for Untrustworthiness’);

- From this point, blacklists and redlists became ubiquitous across government departments, with more than 50 in operation.

- 2017-2018 — Model city trials

- Widespread adoption of regional trials of the social credit system, with 12 such cities in 2017 being classified as ‘model cities’. Perhaps the most prominent example city is Rongchen. The city introduced a comprehensive grading and reward and punishment system. The platform involves collaboration between 142 government departments. Hundreds of positive and negative factors go into the final score, with positive scoring individuals having priority access for finance and licenses.

- In Suzhuo, a collaboration between the city government and Ant Financial with the ‘Osmanthus‘ score was applied to 13 million residents. High scores meant (among other things), public transport and library benefits.⁶

- 2019 — Towards AI

- The State Council released ‘Guiding Opinions on Accelerating the Construction of a Social Credit System and Building a New Credit-based Supervisory Mechanism’. This emphasized the need for big data and artificial intelligence to provide early warning of risky actors in need of extra regulatory attention. It also recognized the need to focus on market regulation.

- At the same time, the document called for improved credit repair mechanisms, enhanced data collection and privacy protections.

- 2020 — Covid-19 implications and further standardization

- In December 2020, a draft of the Social Credit Law was released for internal consultation. There is speculation that the eventual law may look like existing provincial social credit regulations that have been implemented, such as Shanghai’s.

- Covid-19 also saw the China social credit system altered in various ways to recognize the impact of the pandemic. This is discussed in detail below.

How Does China’s Social Credit System Work?

The China social credit system rates individuals based on the aggregation and analysis of data. In some trials, this has involved a single numerical score (usually between 1 and 1000, like a FICO score), or a letter grade (usually from A-D).

This information is acquired from a range of sources including individual businesses (including ‘big tech’) and government entities. Some of the information is ‘siloed’, and accessible only by the individual regional or central government authority. But in many cases, the information is shared with other regulators through a centralized database, such as NCISP.

For example, some of the factors that can be considered in giving a corporate social credit rating include:

- Whether the business has paid taxes on time

- Whether the business maintains necessary licenses

- Whether the business fulfills environmental-protection requirements

- Whether the business meets product quality standards

- Whether the business meets requirements specific to their industry.

It is important to note that businesses’ scores may decrease based on the behavior of their partners. This means enterprises need to think very carefully about who they do business with in China.

Punishments in China’s Social Credit System

As the China social credit system is still in a state of evolution, it is impossible to say with certainty what exactly the negative consequences are. That said, based on those elements that are currently in place, as well as existing regional pilots, potential negative effects of a bad score once fully implemented include:

- Travel bans

- Reports in 2019 indicated that 23 million people have been blacklisted from travelling by plane or train due to low social credit ratings maintained through China’s National Public Credit Information Center. It is reasonable to assume that this will continue as part of China’s social credit system.

- School bans

- The social credit score may prevent students from attending certain universities or schools if their parents have a poor social credit rating. For example, in 2018 a student was denied entry to University due to their father’s presence on a debtor blacklist.

- Reduced employment prospects

- Employers will be able to consult blacklists when making their employment decisions. In addition, it is possible that some positions, such as government jobs, will be restricted to individuals who meet a certain social credit rating.

- Increased scrutiny

- Businesses with poor scores may be subject to more audits or government inspections.

- Public shaming

- In many cases, regulators have encouraged the ‘naming and shaming’ of individuals presented on blacklists. In addition, flow-on effects may make it difficult for businesses with low scores to build relationships with local partners who can be negatively impacted by their partnership.

In addition, businesses of individuals need to consider the negative effects that the actions of a person or business can create for others due to a poor social credit score.

For example, engaging with companies that have a low social credit score (such as those that are ‘blacklisted’) can reduce one’s own social credit score. In addition, if an individual with a poor social credit rating opens a business, the business may automatically begin with a low social credit score.

The majority of megacities and mid-sized cities in China have already implemented a trial period of the social credit system. There are many ways to lose points and lower one’s social credit score, depending on the city where the offense takes place. Some of the more trivial score-lowering actions include:

- An individual not visiting their parents on a frequent basis

- Jaywalking

- Walking a dog without putting it on a leash

- Smoking in a non-smoking zone

- Cheating in online videogames

Some have questioned whether some of these activities and behaviors are bad enough to merit the penalties that result from a low social credit score.

It should be noted that the court system is available for individual’s or corporations to appeal their score.

Blacklists and Redlists in the Chinese Social Credit System

So far we have made several references to the ‘blacklists’ and ‘redlists’ associated with the China social credit system. So what exactly is a blacklist?

China currently has a number of national and regional blacklists based on various types of violations. It is expected that over time, the system of blacklists will be fully integrated with the social credit score.

Businesses can be placed on a blacklist due to a particular violation or because of a poor social credit score. A government notice released in 2016 encourages businesses to consult the blacklist before they hire someone or assign them a contract.

Please note that companies will not be blacklisted automatically for compliance failures. The corporate social credit system also maintains an irregularity list. This list deals with significant (but not yet ‘blacklist’ level), non-compliance.

Presence on this list means the business is in danger of being blacklisted and should quickly take steps to improve its reputation.

The Chinese government utilizes the blacklist in multiple ways. The list itself is frequently being analyzed, with the available information on both its citizens and companies listed in their Master Database working as a template for assigning each person a score.

While the China Blacklisting system is still in its early stages, it is already the most prominent system of its kind worldwide. China has already put this system into action, and has barred thousands of Chinese residents’ rights to buy plane tickets and travel either domestically or abroad. However, most of the blacklisting that has occurred to date has been as a result of violations or misbehavior of companies and the individuals working for them.

In its current iteration, the blacklisting system is highly complex. Instead of having a single blacklist used by the federal government, there are currently hundreds of blacklists being controlled by various state agencies around China. Every agency has its own jurisdiction in which it operates, giving these localized organizations the ability to blacklist individual citizens and companies that operate within their area of authority.

It’s important to note that being blacklisted under one agency’s jurisdiction may leave the affected party subject to blacklisting from the remaining agencies across the country (the level of integration of blacklists differs across the country and between different government departments).

It typically takes 2 to 5 years to be successfully removed from a blacklist, which often has a negative impact on the privileges afforded to those individuals and businesses in society. Early removal from the list is a possibility for some, depending on the severity of the offense and whether the offending party has done enough to rectify the situation in the eyes of the relevant governing body.

In addition to being used as a metric for punishing citizens and companies for violating the country’s guidelines, the social credit system is also intended to be useful in China’s search for signs of potentially harmful behavior before it occurs.

Rewards in China’s Social Credit System

On the other end of the spectrum, there are positives of the social credit system for people and corporations who are determined to be outstanding members of Chinese society. In this context, the opposite of being blacklisted is to be ‘redlisted’ (also spelt ‘red-listed’). Redlisting allows citizens and companies access to certain privileges that will impact their day-to-day lives.

There are a range of rewards for businesses that do well in this regard, including:

- Streamlined administrative procedures. For example, companies that are classified as an ‘Advanced Certificate Enterprise’ may receive faster customs clearance. ‘A-rated’ tax-payers may have their tax returns processed more quickly

- Fewer inspections and audits

- Fast-tracked approvals.

How is Technology Integrated within the Social Credit Score System?

New innovations in technology are poised to play a large role in the country’s social credit system. Artificial Intelligence (AI) facial recognition software is said to be currently utilized in tandem with over 200 million surveillance cameras in China.

Some argue that the purpose of large-scale surveillance measures is to give Chinese officials the ability to track their citizens in every facet of everyday life: In turn providing masses of data to determine whether an act worthy of being blacklisted has occurred.

Along with these physical surveillance measures, the Chinese government continues to track the online behaviors of its citizens. There are a plethora of violations Chinese officials may be looking for, including evidence of writing and sharing anti-government ideologies.

The AI software is able to do the majority of this work on behalf of the government and alert officials when a violation has occurred. The technology has advanced to a place where the AI can identify videos of anti-government protests and block users from viewing them.

Businesses must be cautious when navigating China’s compliance laws as well, as their internet data may be used against them in the event of a violation. Data that reveals a company’s lack of compliance in regards to contractual obligations are factored into and can play a significant role in determining the company’s social credit score.

It is worth noting that, generally speaking, China’s public security system and social credit system are distinct. Currently, blacklists and redlists are created via the manual inputs of officials and there is not yet any full-scale integration between the state’s security apparatus and the social credit system.

What is China’s Corporate Social Credit System?

While the social credit system in China is universal in application, the policy focus to date has been on its application to companies. According to one analysis, 73 percent of policy documents released to date have been focused on the application of social credit in the corporate sector.

The goal of the corporate social credit rating is to combine data from many different sources to provide a public searchable database of companies, and to evaluate and score those companies against a list of compliance criteria.

While the corporate social credit rating is still in a development phase, the goal is to work towards a ‘Comprehensive Public Credit Rating’, which will provide an overall score for companies operating in China.

In the meantime, companies need to use a range of existing databases providing information and evaluations of companies, based on overlapping, yet distinct datasets. The databases can be national, regional, local, and based on particular industries.

Businesses are assessed based on compliance, financial and audit records: More than 33 million businesses in China have been assessed to date.

Important concepts in the corporate social credit system include:

- Grades and ratings. Scores are currently in the development phase (these will be similar to the three-digit credit scores you may already be familiar with in other countries). However, there are four basic letter categories used: A= Excellent; B=Good; C=Average; D=Not sufficient;

- Redlist/Redlisting. As discussed earlier, this is a mechanism to reward companies that are performing well;

- Irregularity list. This lists companies with significant non-compliance. If a company is on this list, the authorities are paying attention to it;

- Blacklisting. Blacklisted companies are classified as heavily distrusted. This categorization can result in your business license being revoked;

- Unified Social Credit Code. This is your company’s unique business identifier across the different databases.

Below we look at how to check your status using a key national database, CreditChina.

How to Check Your Company’s Corporate Social Credit Score using CreditChina

CreditChina is a search tool (only available from a Chinese IP Address), providing a range of information on companies and individuals. Information incorporated into its assessments includes:

- Basic identifying information for the company, including the company’s Unified Social Credit Code and permits held;

- Any applicable administrative penalties;

- Any payment defaults recognized by the Courts;

- Any instances of tax evasion and fraud;

- Instances of illegal importing or exporting;

- Unpaid wages

There are several sub-databases provided, including one relating to redlisted companies, one for blacklisted companies, and one for companies with irregularities.

To proceed with checking your rating or score in CreditChina go to the CreditChina homepage as shown below:

Then, take the following steps:

Click on the ‘Credit’ tab (first item in the list)

Search for the company either by name, or by Unified Social Credit Code;

The record that you see, will show:

- Any administrative permits held by the company;

- Any administrative penalties applied to the company;

- The presence of the company on redlists;

- The presence of the company on blacklists;

- The presence of the company on any irregularity list.

If you find ‘negative entries’ (presence on a blacklist or irregularity list), you should seek advice on how to improve your situation. Or, if you think there has been an error, you can make a complaint seeking directly to the authorities seeking a correction of your record.

How to Check the Status or Rating of your Company Using Other Databases

NECIPS is another national database, arguably not as user-friendly as CreditChina. It has the most comprehensive set of information on social credit system records, as it collects data from the most government sources. In addition, NECIPS:

- Provides more comprehensive identification data relating to the company;

- Allows for reporting on social credit system issues directly to the authorities.

Companies should also check local databases in the areas where they are located, as well as any subject matter-specific databases. These databases include:

- The tax database that lists when companies have excellent tax-filing and payment practices;

- The environmental regulatory database;

- A customs database;

- A procurement database.

Why Is the Corporate Social Credit System Important For Your Company?

The corporate social credit system is important for two reasons. First, you need to know who you are doing business with in China. The corporate social credit rating lets you look up potential business partners and collaborators and check their reliability. Second, understanding the corporate social credit system is essential for your own business. In order for other companies and the government to be willing to engage with you, you need to continually demonstrate that you are a compliant entity.

Looking up your corporate credit rating on the available databases is essential in order to check that you are on track. We recommend that you seek professional advice and assistance to ensure that your company can increase its ‘positive’ credit entries and decrease the number of ‘negative’ entries.

What Is the Difference Between Alibaba-Affiliated ‘Sesame Credit’ and the China Social Credit Rating?

The China social credit system is often confused with existing credit ratings provided by private credit providers. It is commonly likened to Sesame (Zhima) Credit, which is operated by Alibaba’s Ant Financial.

Note, Sesame Credit has no connection to ‘Credit Sesame’, a US-based credit and loan company.

Whilst Alibaba was involved in constructing infrastructure mechanisms for the social credit system (Alongside other Chinese ‘big tech’ firms such as Tencent and Baihe), Sesame Credit is an optional platform. It exists for the use of Alibaba group customers. Rewards include streamlined access to loans from Ant Financial, and an enhanced profile for operating on other Alibaba Group sites. It is distinguished also by its use for individuals, as opposed to businesses.

The Sesame Credit model takes into account a range of information including the individual’s payment history and debt, their ability to fulfill contractual obligations, and their personal characteristics. In this respect, Sesame Credit works in a similar way to some credit systems in the United States. For example, while the most common form of credit score in the US, the FICO score, does not take into account personal characteristics, lenders often take those factors into account when implementing those scores.

How to Prepare for the Implementation of China’s Social Credit Points System?

While some valid concerns have been expressed about the trials of the social credit system so far, the potential benefits for foreign companies looking to extend or establish their operations in China cannot be underestimated. If it works as intended, the social credit system will mean:

- A leveled playing field against domestic companies. Through publicly accessible databases, foreign companies will be able to know that they are doing business with a reliable partner. This is especially important for enterprises when they first enter the China market. To date, this information was primarily known by local Chinese companies ‘in the know’;

- Standardized credit ratings across China. Foreign companies will be able to have confidence that a rating given to a company in Shanghai will be based on the same factors as a credit rating given in Shenzhen.

In preparation for the implementation of the China social credit system, it is imperative that businesses both foreign and domestic understand which information they need to provide to authorities. Once this information is identified, businesses should conduct an internal audit which will allow full compliance with the necessary regulations.

In addition to these measures, businesses should prepare a supply chain audit and confirm that any business partners meet social credit guidelines.

Businesses should also analyze their IT and data security, as the transmission of this data to government bodies will need to be undertaken.

While not mandatory, businesses should assess whether their operations are conducive to the advancement of government policies. This can include measures of corporate social responsibility that align with government priorities and wider policy initiatives.

What Is the Public Perception of the Social Credit System?

As the social credit system is relatively new and unfamiliar to individuals and businesses from other countries, it may seem ‘scary’. However, a significant degree of reporting in English-language media has been based on linguistic confusions and policy proposals that have not yet been implemented. For example, businesses do not currently get penalized for ‘frivolous spending’, as has been widely reported.

As an example, see the reporting from NBC in 2019 below.

In many respects, a credit score in the United States, for example, can have just as serious consequences for individuals and businesses, as China’s social credit system: For example, access to transport can be seriously curtailed in the US due to a poor credit rating through higher insurance premiums and limited access to car loans.

In 2017, CNBC looked at the similarities between the China social credit system and FICO scores in the US. One commentator quoted there, Forrest Zhang, Professor of Sociology and Singapore Management University, commented: “From what has been outlined in the official sources, there is nothing more intrusive than what is commonly done in the West”.

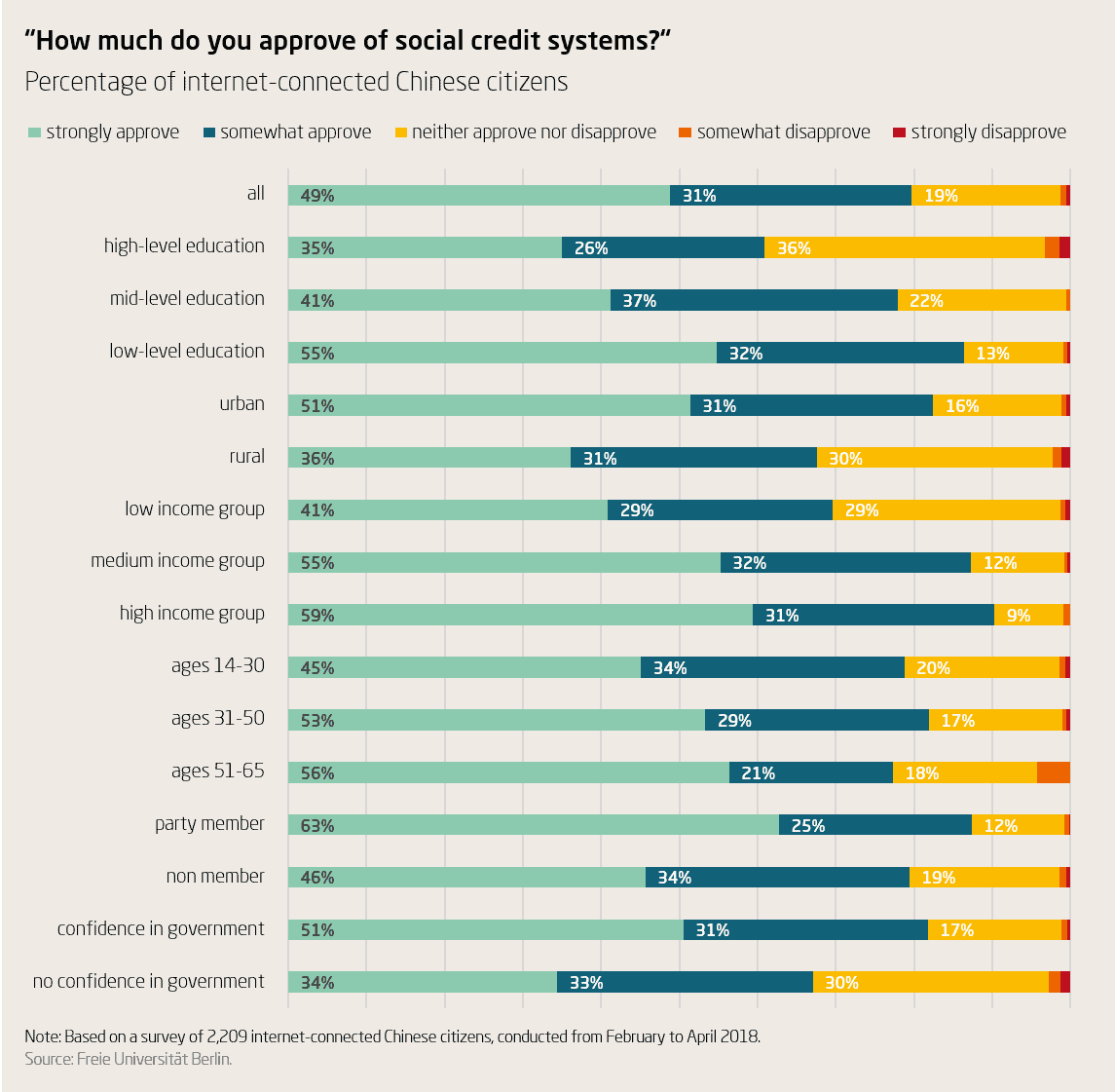

Although there has been substantial resistance to the social credit system from a global perspective, it appears that most Chinese citizens approve of the system. In addition, those most familiar with the social credit system and how it is being implemented, citizens and businesses in China, are widely supportive of the system.

In one peer-reviewed study, 80% of respondents either somewhat approved or strongly approved of social credit scores. Just 1% of participants reported either strong or some degree of disapproval in the system.

While not all studies have shown such a high level of support for the system within China, all show a broad degree of support. See, for example, the study below.

It is important to note that this survey only represents Chinese internet users that participated in the survey and is not necessarily a representation of how the country feels as a whole.

From what has been outlined in the official sources, there is nothing more intrusive than what is commonly done in the West.

Forrest Zhang, Professor of Sociology, Singapore Management University

Are There Overseas Equivalents to the Social Credit System?

As noted above, it has been suggested that the social credit system is not so different from forms of citizen evaluation in other countries, such as the United States. Is this true? Below we consider some of the wide-scale ‘trust’ and big data programs in other countries, and consider how they compare with elements of the China social credit system:

- Australia

- One of Australia’s biggest immigrant groups are New Zealanders, who are entitled to live and work in Australia for life under the terms of a ‘special category visa’, usually awarded on arrival. This visa has a ‘good character’ test which has been used to deport those resident in Australia for decades, entirely at the discretion of officials. In a recent case, this was used to detain and deport a 15-year-old child. Arguably, this has some similarities with the way the China social credit system can affect freedom of movement based on anti-social behavior.

- The ‘ParentsNext’ welfare program provides payments for single mothers. To qualify, recipients must verify every week that they have undertaken certain activities with their children, such as attending swimming lessons or going to the library. This has some similarities with the capability of the China social credit system to penalize and reward individuals for private family activities.

- Trustbond is a private Australian company which uses social media data to come up with a ‘trust score’. This can in turn can be used to replace traditional cash bond payments for potential renters. This has some some similarities with the way in which trials of the social credit system have used social media data to improve overall scores.

- The city council in the city of Darwin trialled technology recording people’s movements from cellphone data within the city centre. When a ‘ping’ is received at the control centre, surveillance cameras can identify the individual and Police can be notified. This has similarities with the camera surveillance aspects of the China social credit system.

- Germany

- Germany’s expansive credit rating system has a significant impact on individual liberties. The ‘SCHUFA’ score (similar in some ways to the ‘FICO’ score in the United States) is necessary for renting or buying a house in Germany, borrowing, or receiving goods on credit. While the details of the score are kept secret in the interests of commercial secrecy, it has been claimed that being in a low-income area or having low-score neighbors could negatively affect your score.

- It is clear that there are analogies here with the way in which the China social credit system can punish perceived ‘anti-social’ behaviors. Some would argue that the German system leaves these scores even more opaque, by allowing these decisions to be made entirely by private companies.

- Similarly, some health insurance providers (health insurance is compulsory in Germany), use fitness data through apps to offer reduced insurance premiums. This has similarities with the way in which the China social credit score prioritizes, and gives a higher score to, pro-social behaviors.

- India

- India’s unique identification program known as ‘Aadhaar’, provides each resident with a 12-digit number and records their demographic and biometric data, including fingerprints and iris scans. The program began in 2009 as a voluntary system, but now covers 99 percent of the population.

- Its original purpose was to ensure access to welfare programs, but concerns have been raised about its use by law enforcement, as well as illegal access for commercial purposes. This has some similarities with the mass gathering of surveillance data in some trials of the China social credit system.

As is evident from the examples given above, many elements of the China social credit score are already implemented in other countries.

What is distinct about China’s system is its sheer size and breadth, as well as an overall Government strategy and direction around the collection and use of big data.

Progress on the China Social Credit System in 2020-2024

2020 was the original target year for implementation of the China social credit system. However, a range of factors, including the impact of Covid-19, delayed the full establishment of the system.

Throughout the course of 2020, there were four significant variations to the social credit system in response to the pandemic. Note, these changes were not applied nationally, but regionally and by municipal governments, depending on how they were impacted by the Pandemic. These included:

- 1. Exemptions from Penalties

- Individuals or corporations that could show that breaches of contractual or tax obligations were due to Covid-19, were made exempt from the penalties for doing so.

- 2. Social Credit Rewards for Entities Contributing to Containment of Covid-19

- Companies which could demonstrate a ‘decisive’ contribution to the fight against Covid-19 (such as those donating medical supplies) were eligible for certain rewards. This included inclusion on a ‘green list’ which streamlines administrative issues for that business.

- 3. Penalties for Companies Exploiting the Pandemic or Breaking Restrictions

- Any businesses that could be demonstrated to have exploited the pandemic (such as engaging in price-gouging of essential materials), or the breaching of Quarantine and other Coronavirus restrictions, were penalized.

- 4. Simplified Loan-Granting Procedures

- In certain cases, individuals or entities in industries heavily impacted by Covid-19 had simplified and speedier access to credit.

January 2021 saw the NDRC release a national guiding document for credit information reporting. This is designed to encourage the standardization of credit information reporting between provinces.

In addition, the latest 5-year ‘Plan on Building the Rule of Law in China (2020–2025)‘ sets out a vision for the connection between technology and law, as well as an intention to progress social credit legislation. As of mid-2021, this legislation is still in draft form, being considered by government departments.

In July 2021, two draft documents were released in relation to the social credit system: The National Social Credit Information Basic Catalog and the National Basic List of Punishment Measures for Untrustworthiness.

This includes a list of the information that is to be collected as part of the system, covering information related to:

- Registration;

- Judicial decisions and arbitration;

- Administrative determinations;

- Professional titles and qualifications;

- Abnormal business activities;

- Being on the list of “seriously untrustworthy subjects”;

- Contractual performance;

- Credit commitments and their fulfillment;

- Credit evaluation results;

- Honesty and trustworthiness;

- Credit information from market entities.

On March 29 2022, a new policy document was released, suggesting a shift in emphasis towards social wellbeing and environmental issues for the social credit system. Opinions on Promoting the Construction of a Social Credit System with High-Quality Development and Promoting the Formation of a New Development Pattern proposes:

- Mechanisms to improve consumer trust, such as a product traceability system, and stopping the production of counterfeit goods

- Supporting labor rights by penalizing fraud in social insurance benefits, and affordable housing entitlements

- Credit for complying with environmental protections and soil and water conservation.

China Social Credit System — Our Take

The China social credit system so far, is a collection of disparate rating systems, largely administered by central and local government agencies. While a comprehensive individual ‘social credit score’ was originally envisaged, so far such a score has only been rolled out on a corporate level.

So far, it appears as though the Chinese Government is slowing down on its intention to roll out a full system, and is more focused on its application to corporate compliance.

By working with a local expert like Horizons, you can identify the type of information that you will need to provide to authorities, receive an internal audit to ensure compliance and access due diligence on potential business partners.

Frequently Asked Questions

It depends. If a foreign individual operates or works for a business entity established in China, such as a Wholly Foreign-Owned Enterprise (WFOE), the enterprise may have a social credit score already: It depends on which part of China they are operating in and their industry.

Note, corporate social credit scores currently only apply to enterprises with a business registered in China: This could include subsidiaries, branches and joint ventures, among other business forms.

There is no difference: The two terms are used interchangeably. Individuals and corporations may be assigned social credit scores or ratings which are numerical (often between 0 and 1000), or a letter grade (often from A to D).

It is worth noting, however, that there is more to the social credit system than scores or ratings. Perhaps more prominent are the blacklists and redlists that need not line up with a social credit score or rating.

No. An in-depth analysis of material available to date indicates that local Chinese firms have not been given preferential treatment.

Furthermore, there is no indication that government and government-associated entities have received special treatment: That same study showed 1,391 state-owned enterprises are on the Supreme People’s defaulters blacklist.

In an episode of Netflix’s Black Mirror, citizens were given a rating by others of between 1 and 5, based on social interactions. Access to opportunity in that society depends on one’s rating, with higher ratings providing access to flights, rental cars and apartments.

The China social credit system does not have much in common with the ‘Nosedive system’. Crucial to the China social credit system are publicly released criteria for rating individuals: Individuals have never been ranked based simply on the opinions or perceptions of other people.

While it is true that in some trials of the social credit system individuals have had access to travel restricted, this is common in credit systems in other countries as well. For example, it is common for rental car companies in the United States to impose minimum FICO scores for renting vehicles.

It is sometimes imagined that the China social credit system automatically creates entries for individuals based on surveillance footage or other digital streams. This is not currently the case. All entries into an individual’s china social credit rating are manually entered and overseen by officials.

Currently, there is no one ‘social credit score’ that applies across China and to all individuals. There are many different social credit scores depending on the region or city in which the person is located and the services they use.

This means that there is no single set of factors that the social credit score depends on. For example:

- Corporate social credit scores are partly dependent partly on filing taxes correctly and on time

- In the 2016 Nanjing pilot, willingness to donate blood and work ethic were taken into account in calculating social credit scores

- In the recent Rongchen pilot, traffic violations reduced the social credit score while donating to charities increased the score.

No. However, many aspects of China’s social credit system have similarities with US scoring and penalty systems including:

- The Hollywood blacklist. In the 1940s and 1950s, a committee of the U.S. House of Representatives, the House Un-American Activities Committee, spearheaded a blacklist of entertainment industry figures who were perceived as having communist sympathies. Presence on the blacklist ruled an individual out of working with major studios and entertainment companies;

- FICO credit scores. These numerical scores determine an individual’s access to financial credit;

- Tech rating systems. The scoring systems developed by Uber, Airbnb and the like, radically affect an individual’s access to accommodation and transport based on their numerical score through use of the app.

Generally speaking, no. An individual who has never been in China is unlikely to have a social credit score.

However, foreign individuals resident in China are likely to be evaluated in the same way that Chinese nationals would be.

Note also that foreign individuals who control, or are managers of, China-based enterprises could be captured in the social credit system.

No. The economic theory of social credit concerns the redistribution of capital (and thus credit) to producers, rather than industry and financial institutions. This theory, developed by economist C.H. Douglas, was adopted by political parties in various English-speaking countries, especially Canada, where social credit parties were in Government in British Columbia and Alberta.

This has no connection to the China social credit system, with the use of the term ‘social credit’ being a coincidence of translation.

They are completely different. The China social security system concerns the set of benefits and entitlements (including healthcare, unemployment insurance and compensation for workplace injury) that Chinese workers are entitled to.

There is no proposal that an individual’s social credit score will affect their access to social security.

Individuals and companies can build and improve their social credit score in various ways, depending on their location and industry.

One way all companies can do this is by endeavoring to end up on ‘red-lists’. For example, the State Tax Administration (STA) redlists companies where they have paid their taxes in full and on time, in the prior two years, and they have not been blacklisted by any other body.

For individuals, it will be important to look at score-building criteria within the municipality or region. For example, in some cities, volunteering for good social or environmental causes will increase the social credit score.

If a company or an individual has ended up with a poor credit score, they will need to take steps to repair that score. If a company or individual believes that they have been incorrectly black-listed or scored, they may also make an appeal.

Note, however, that while national policy documents on credit repair have been released, there is currently no nationally consistent process in place.

In general, any blacklisted company will remain on that list for a mandatory period, which can be up to five years. Blacklisted companies can seek the help of accredited credit repair agencies in being removed from a blacklist.

In many cases, government-approved courses can be taken in order to repair a social credit score.

Skynet is the Chinese network of government-monitored surveillance cameras operating in 16 provinces. Facial recognition software is applied, allowing identification of individuals with a high degree of accuracy.

Currently, there is no evidence that Skynet has been integrated with the China social credit system.

The corporate taxpayer rating, a component of the China Social Credit System, evaluates the taxpaying behavior of corporate entities in China.

On the basis of taxpaying activity over the period, corporations are given a rating each April. Corporations are scored with an A, B, M, C, or D grade.

Grade A, the best score, means a score of 90 points and above, while Type D is the poorest rating, for scores below 40. Type M is reserved for new taxpayers.

In broad terms, corporations are graded on their honesty and transparency in their filings, as well as timeliness. Grade A taxpayers will be subject to streamlined administrative procedures, whereas Grade D taxpayers are subject to increased scrutiny in matters such as returns and refund applications.

Endnotes

¹ For an in-depth discussion of the concepts underlying China social credit see Zhang, Chenchen (2020). “Governing (through) trustworthiness: technologies of power and subjectification in China’s social credit system. Critical Asian Studies. See also Blomberg, Marianne von (2020). The Social Credit System and China’s Rule of Law. 10.1007/978-3-658-29653-7_6.

² Yu Jingming, Lin Junyue, Sun Jie (2000). National Credit Management System. Beijing: Social Sciences Academic Press.

³ Innovation Centre Denmark, Shanghai. (2018). ‘Social credit & big data trends IN CHINA’.

⁴ For an extensive discussion of the Suining trial see Mac Sithigh, Daithi and Siems, Mathias. (2019). ‘The Chinese Social Credit System: A Model for Other Countries?’. EUI Department of Law Research Paper No. 2019/01, Available at SSRN: https://ssrn.com/abstract=331008.

⁵ For further discussion see Mo Chen and Jens Grossklags (2020). ‘An Analysis of the Current State of the Consumer Credit Reporting System in China‘. Proceedings on Privacy Enhancing Technologies. (4):89–110.

⁶ For an in-depth discussion of the Rongchen and Suzhou trials see Innovation Centre Denmark, Shanghai. (2018). ‘Social credit & big data trends IN CHINA’.

⁷Brussee, Vincent (2023). Social Credit: The Warring States of China’s Emerging Data Empire. Singapore: Palgrave MacMillan.